Award-winning PDF software

Coral Springs Florida Form 982: What You Should Know

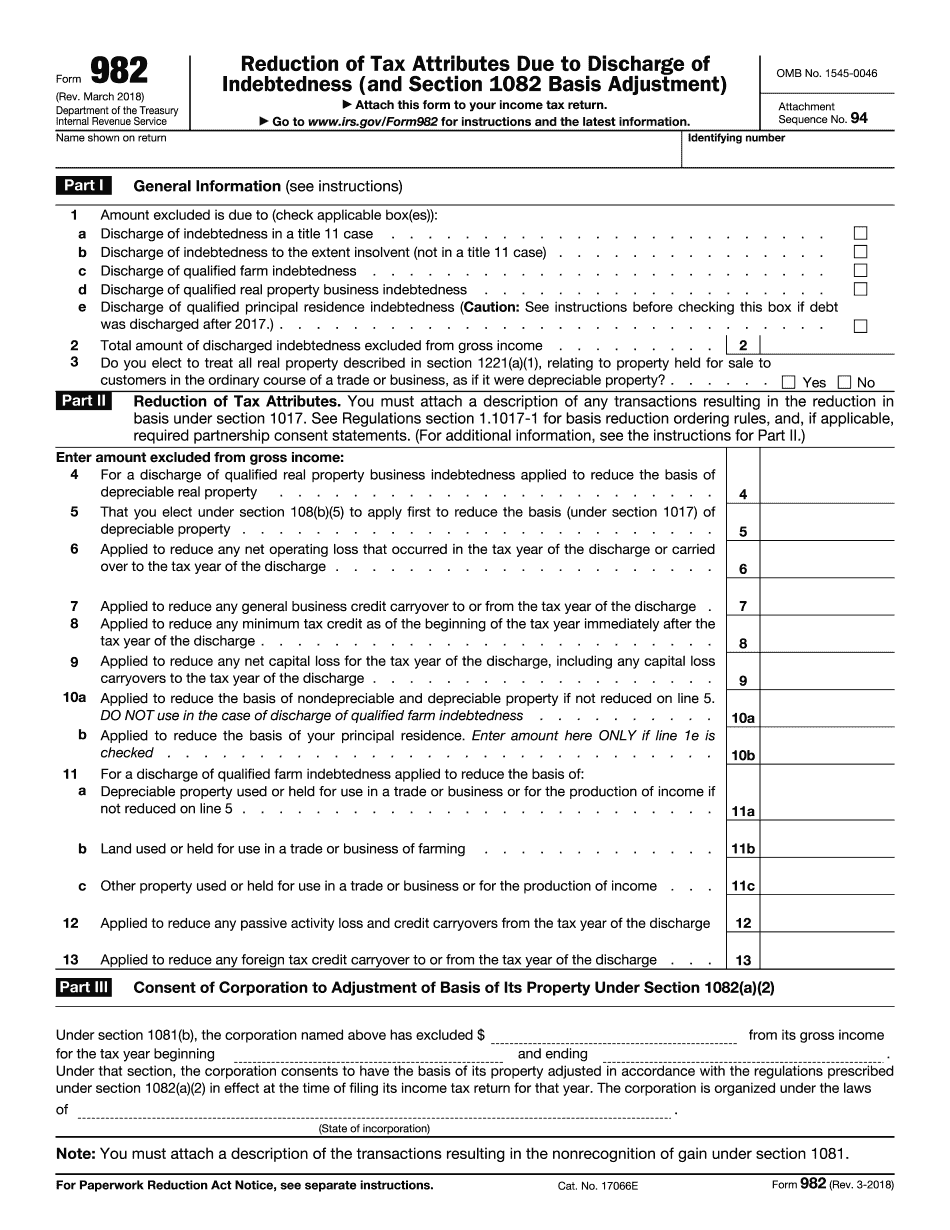

Part 1: What are Losses and Gain? Part 2: How do Gain and Losses Differ? Part 3: What Is a Depreciation Property? Part 4: Selling the Home (or Any Other Investment Property) Part 5: Closing the Home Questions on Section 108 What Are Losses or Gains? The basic concept of a capital loss or gain is described in section 2 (a) but in general, a loss or gain is the difference between the amount of capital gains or losses and the adjusted basis of the property. Generally, most capital gain or loss is not taxable unless you sell the asset. But the IRS allows capital gains and losses that exceed your adjusted basis to be taxed as ordinary income (which is taxed at your ordinary income rate). See capital gains and losses on Form 4040. If you dispose of a qualified investment property before having used it for 10 of the preceding tax years, you do not have to pay federal taxes on the qualified investment property until after you use the equipment for 10 years. However, if you are not eligible to receive a 10-year exclusion or deduction, you can deduct the capital loss or gain that you would have reported as ordinary income on your tax return if you have the exclusion. See section 1 of Pub. 15-A for information on the tax treatment of the capital gain or loss from a sale. So that's how capital gains or losses and a depreciable asset (or anything else with an adjusted basis of over 25,000) are treated. However, the gain or loss on a qualifying real property or qualified small business property, and any gain or loss on sale or other disposition of any property is considered a “capital asset.” The IRS refers to this as property used in carrying on the qualified investment business that you are a partner in. If a business partner sells all or a part of that partnership's business, the capital asset in the case of a partner that sells the business must be disposed of for a gain before any gain is recognized. If all partners, or about 80% of the partnership, were not related at the time of the sale, no gain may be recognized. See Capital Asset to be Acquired, later, for more information on property that is not capital property. The difference between the total basis and the adjusted basis is the basis of the asset. You can do a short sale before the end of the tax year that you held the asset.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Coral Springs Florida Form 982, keep away from glitches and furnish it inside a timely method:

How to complete a Coral Springs Florida Form 982?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Coral Springs Florida Form 982 aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Coral Springs Florida Form 982 from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.